Europe’s water industry is shifting towards a more sustainable and resilient future by leveraging national policy incentives, innovative financing methods, and advancements in digital technology.

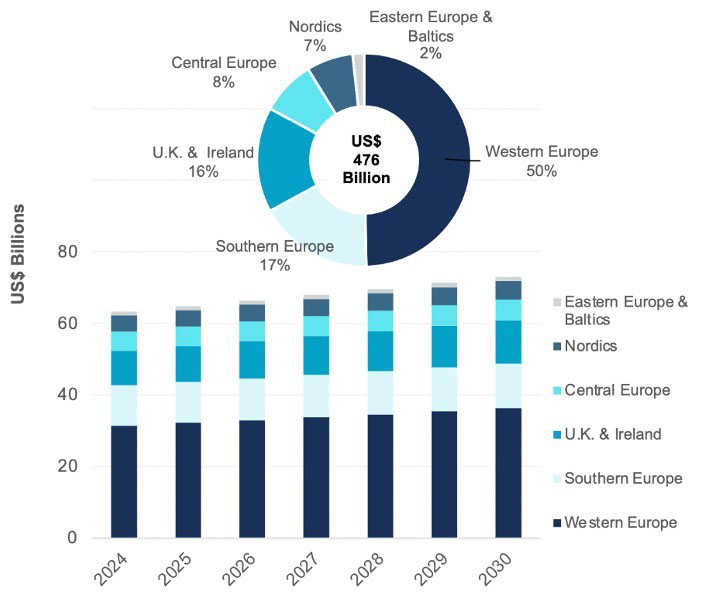

Bluefield Research projects a total of US$476 billion in capital expenditure (CAPEX) for water and wastewater infrastructure in Europe from 2024 to 2030, with notable regional variations. The market is anticipated to grow by 2% annually, reaching around US$75 billion by 2030, as outlined in the report “Europe Municipal Water & Wastewater: CAPEX Market Forecasts, 2024–2030.”

Zineb Moumen, Europe Water Market Analyst at Bluefield Research, notes that Europe’s water sector has historically shown stability but is now at a pivotal juncture. Governments are embracing more forward-looking policies to tackle long-standing water challenges like population growth, drought, and leakage. The European Green Deal, a groundbreaking commitment to climate neutrality, aims to achieve zero net greenhouse gas emissions by 2050, encouraging water utilities to invest in more efficient and sustainable practices.

A key component of the European Green Deal is the Urban Water and Wastewater Treatment Directive (UWWTD), which establishes a common set of standards for managing and treating water resources. This directive will underpin stricter regulations on water quality, including addressing PFAS, emerging contaminants, and nitrogen levels in water. These regulations will compel water and wastewater utilities to address growing economic, environmental, and regulatory pressures.

Water scarcity poses significant challenges to various regions, with droughts extending beyond the usual summer period. Catalonia, Spain has implemented a Water Agency Drought Plan to reduce average daily consumption to 160 liters per person.

The region has allocated funds for drilling to access underground water sources and for infrastructure improvements to enhance water supply resilience and avoid extreme measures like water shipments. In the U.K., utilities are facing public and regulatory scrutiny due to poor environmental performance and high leakage rates. These utilities are focusing on enhancing water security, reducing leaks, and improving wastewater management by 2030.

“It is a critical time, as U.K. utilities are currently ramping up for the Asset Management Planning Cycle. AMP8, as it is termed, features an 86% increase from the last investment cycle, thereby doubling the utilities’ capital investments in the sector by 2025,” says Moumen.

Affordability, financial sustainability, and securing funding for utilities in Europe continue to be a significant concern. Europe stands out for its diverse sources of funding for water infrastructure projects, including national budgets, the EU Cohesion Fund, and sometimes private investors. While this blended funding approach has enhanced the scope and pace of infrastructure development, a central issue persists: Who will foot the bill?

“To establish a sound financial framework, the water and wastewater sectors need to strike the right balance between revenue from water usage, fees, tariffs, subsidies, fundraising, and private investments,” explains Moumen.

The German government, in particular, acknowledges the necessity of substantial investments to bolster the modernization of the water industry and its resilience to climate change. Bluefield’s assessment reveals that Germany’s strategic blueprint encompasses 78 specific actions to be executed through a combination of diverse funding sources and regulatory measures.

Countries in Eastern Europe, grappling with aging water infrastructure challenges, are specifically focusing on revitalization and replacement strategies. For instance, Romania—where 30% of the populace is awaiting access to public water supply and 47% is yet to be linked to a sewer network—must adhere to a series of water quality, treatment, and management directives under the UWWTD. According to Bluefield’s analysis, Romania ranks among the top five rapidly expanding European water markets, with €458 million (US$54 million) in annual CAPEX planned until 2030.

Although significant policy shifts will require time to navigate through national legislation in member states, water and wastewater system operators throughout Europe must persist in investing in the essential assets that underpin the sector.

“From the upcoming EU Parliament elections in June 2024 to the evolving PFAS regulations, these policies and initiatives are poised to have profound implications for the future of water and wastewater management,” Moumen emphasizes.

Source :Bluefield Research